Techfoliance is back on the road to meet Fintech actors across the world. We want to highlight emerging trends to better understand the future of finance. In the spotlight: Lithuania.

Lithuania now position itself as an alternative choice for those considering entry to the European market, diversifying the risk of accessing the single market after BREXIT and FinTech start-ups.

Key figures

The number of potential “Digital Payments” users is expected to amount to 1.9m by 2020.

Transaction Value in the “FinTech” market amounts to US$1,182m in 2016.

The Bank of Lithuania is to grant a license for a specialised bank within 6 months after submission of all required documents (maximum terms 12 months).

Easy set up of companies; Lithuania is #1 in Technological Readiness in the CEE; nearly 100% proficiency in English among young professionals.

The passporting notification procedures executed via the Bank of Lithuania might take 1 (for exercising the freedom to provide services) or 3 months (for establishment of branches in other EEA member state).

Population: 2,9 million people.

Legal and regulatory framework for Fintech in Lithuania

Payments and e-money licensing (article #1):

• Fast licensing – payments and e-money license in 3 months

• Sandbox – no regulatory sanctions for start-ups during their first year of operation

• All payment and e-money institutions located in Lithuania can allocate their own IBAN numbers and access to SEPA payments

• Instant payments (SEPA-MMS) to be implemented under the National Payments Strategy by the end of 2017

New framework for specialised banks (article #2):

• A new framework for so called specialised banks to be effective as of January 2017

• Specialised banks will be eligible to the EU passport and require only 1 million EUR initial capital

P2P and crowdfunding regulation (article #3):

• P2P regulation is in place

• The Law on Crowdfunding will come into effect as of December 2016

• Remote client verification is allowed as of November 2016

The success of Fintech start-ups relies on two main factors: customer confidence and regulatory adoption. No surprise, I agree. But let’s see what it really means!

On one hand, Fintech can survive only if its technology inspires confidence and trust to customers and authorities. On the other hand, the industry, like any other financial industry, can be sustainable only if the regulators work on a streamlined legislation.

I believe that regulation should not be a barrier. If you are thinking to enter the Fintech market (yes, it is still possible!), I suggest that you start focusing on the actual market demand, then you target where it is better to scale your business and finally you analyze the regulatory framework of the country.

Obviously London is a major city to consider for many reasons that you probably already know: leading financial center, easy access to capital, advanced infrastructures for talented people, and a truly diverse environment. I believe the latters, the diversity of the city and its talent pool coming from everywhere will greatly maintain London as a leading Fintech hub, Brexit or not.

A good illustration of that is the “Sandbox” created by the FCA (Financial Conduct Authority) dedicated to early-stage Fintech start-ups. The idea behind this initiative is to have a ‘safe space’ and flexible regulatory framework in which businesses can test innovative products and services, business models and delivery mechanisms without being asked to comply with all the regulatory standards.

This approach has at least two effects on a short term perspective. Putting traditional banks in a situation where they have to accelerate their digital transformation. Putting other European regulators in an uncomfortable position where they need to react and take this case seriously (i.e. ‘Autorité des Marchés Financiers’ – AMF in France). As a result, we clearly assist to an unprecedented race between European regulators whose mission is now to make their country the new capital of Fintech in Europe.

But the fact that fintech hubs are competing against each other is a good thing for the European ecosystem. It is indeed the guarantee to make this nascent and innovative industry grow over time.

Given the actual positive state of Fintech regulation in Europe, I strongly recommand that you start focusing on the market demand, rather than the regulatory framework. Remember that the success of fintech is based at least on four attributes: Talent, Capital, Policy, and Demand.

Interestingly, some countries have created ‘special forces’ like in the Netherlands with the ‘Ministry of startups’ or Luxembourg with “Luxinnovation“. Other countries like Abu Dhabi are also planning to set-up such initiatives.

Each month, our team pick-up five figures on Fintech that you must know to better understand the magnitude of the disruption going on in the financial world.

This month, we highlight India as a start-up nation, Fintech adoption in France, FCA regulation, Challenger Banks and millennials and Fintech:

FINTECH FIGURES OF THE MONTH

India will be home to 10,500 start-ups by 2020 employing over 2,10,000 people and Fintech, Healthtech, Edutech, data analytics, B2B commerce and artificial intelligence will contribute the most.

In 2016, 72% of French people had never used a Fintech whereas almost 30% of them say they don’t trust their bank anymore.

The FCA regulates ~56,000 firms providing financial products and services to both UK and international customers.

Top 5 countries forChallenger Banks: UK (40), India (8), USA (5), France (4), Germany (3)

72% of millennials would be likely to bank with non-financial services companies with which they do business, compared to 27% for those over 55.

Techfoliance identified the most popular Fintech influencers on the social media in Belgium. The ranking has been made in partnership with Fintech Belgium.

We based our analysis on the klout score that calculates the influence of a person regarding Fintech topics in Belgium.

According to a recent study published by the consulting firm EY, Belgium appears to be an ‘unexpected ideal hub for Fintech‘. It is shown that Belgium has strong Fintech adoption from consumers, especially with payment solutions; it has a geographic advantage compared to its peers to scale to other markets, an entrepreneurial spirit with talented people and more money is being invested into Fintech companies.

Please find below an overview of the 20 most active people in Fintech in Belgium on the social media:

Please keep in mind that this is not an exhaustive list, there are many more people that are contributing directly or indirectly to the Belgian Fintech ecosystem.

Last update: 26 October 2016

Rank

Picture

Name

Role

Twitter Followers

Klout Score

Change

1

Geert Noels

Co-founder at Econopolis

62 900

71

0

2

Koen Vanderhoydonk

Co-founder at The Financial Think Tank

15 600

62

0

3

Bart Becks

Founder at angel.me

10 100

62

0

4

Toon Vanagt

Co-founder at data.be and Fintech Belgium

6 895

60

0

5

Vincent Vanderbeck

Digital Entrepreneur

820

57

0

6

Eric Rodriguez

Co-founder & CTO at data.be

4 698

54

0

7

Grietje Vermoortele

Customer Experience at ING Belgium

2 038

54

0

8

Silvan Schumacher

Co-founder & CEO at Swanest

12 500

53

0

9

Nicolas Bindels

Co-founder at Swanest

13 500

52

0

10

Edouard Estour

CMO at Scaled Risk

1 665

52

0

11

Xavier Corman

Co-founder & CEO at edebex.com

1 671

51

0

12

Youri Tolstoy

Co-founder at Swanest

14 300

50

0

13

Pēteris Zilgalvis

European Commission

1 680

50

0

14

Damien Guermonprez

CEO at Lemon Way and Business Angel

1 270

50

0

15

Raymond Frenken

Head of Communications at European Banking Federation

954

49

0

16

Kris Vandenberk

Early-stage VC investor

1 825

48

0

17

Roderik van der Veer

Founder Blockchain Vlaanderen

1 260

48

0

18

Dominique Wroblewski

COO at Look&Fin

4 409

47

0

19

Fabian Vandenreydt

Global Head of Securities Markets at Innotribe and The SWIFT Institute

1 812

47

0

20

Jurgen Ingels

Managing Director at Smartfin Capital

1 044

44

0

And because we strongly believe in FinTech diversity and the power of women in financial technologies, we would like to add few names of women who are contributing directly or indirectly to the Belgian Fintech ecosystem:

Tine Holvoet – Senior Research Associate at Vlerick BS

Karen Boers – Startups.be and European Startup Network

Please, feel free to add more women in the comments below!

About Fintech Belgium:

FinTech Belgium is the first and biggest community of Fintechers in Belgium gathering professionals, startup entrepreneurs and investors interested in disruptive business models and new technology for the financial industry. Quarterly fintech event are organized in Brussels with all Belgian members.

We are in a situation where consumers around the world have access to more options than ever thanks to the rise of mobile technologies.

The rising tide of millennials is expecting more personalized and convenient services. The reality is that people are more likely to ask their friends and family for financial advice through social networks for example than to call their bank advisor.

While Fintech covers a diverse array of companies, business models and technologies, companies generally fall into several key verticals, including: Personal finance/Asset management, Money transfer/remittance, Blockchain/Bitcoin, Crowdfunding and Insurance tech.

Over the past year, there has been a shift since banks moved from seeing Fintech companies as disruptors to co-creators. Banks are increasingly collaborating with Fintech start-ups to embed new services and technologies that improve the customer experience and drive efficiency. For example, the Fintech & Payments Association of Ireland was founded in September and is already making tremendous progress bringing together Fintechs, financial institutions, policy makers and government to drive solutions and promote growth together. For many, major tech giants such as Google and Apple are now considered as the biggest threat than Fintech startups, pushing banks to work with the latter.

I strongly believe that regulators are very open to new alternatives when dealing with financial services. Sure, regulators need to measure the risks, but I don’t think regulation will be a barrier for the adoption of new technologies.

For the coming years, the Fintech ecosystem is expected to grow mostly because other monetary and macroeconomic issues in Europe settle down. At the same time, insurTech as an industry is likely to skyrocket, with many insurance companies in Europe ripe for the same levels of disruption than the banking sector (Solvency II in Europe).

Wealthfront is a market leader among automated investment advisors, also known as “robo-advisors”, which are a disruptive force in the wealth management and financial advisory industry.

The company’s mission statement, “Everyone deserves sophisticated financial advice”, sums up the essence of their value proposition, which is to make financial advisory services accessible to everyone. Historically, these services were restricted to wealthy individuals because of the associated costs.

Wealthfront addresses this problem on all three levels of Doblin’s framework of innovation.

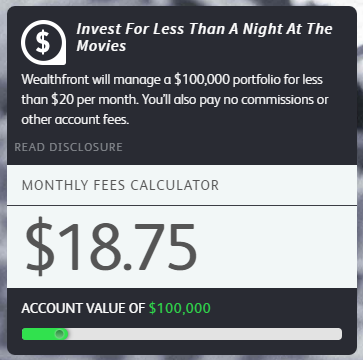

Wealthfront monthly fees calculator

On the configuration and offering level, Wealthfront has managed to break the cost structure of the industry by streamlining and widely automating processes. Using an investment strategy that is based on algorithms and cost effective ETF products, Wealthfront is able to be cheaper than its traditional competitors while still offering their clients portfolios that are tailored to individual risk/return profiles.

At the same time, on the experience side, Wealthfront has created an extremely appealing interface and combined it with a high level of service.

Their innovative customer experience includes a very user-friendly on-boarding process (ex: 5-minute setup; no minimum withdrawals/deposits; automatic deposits) and also offers product related services like automated portfolio rebalancing or tax-loss harvesting.

The client segment that Wealthfront aims to address is rather large at first sight. In general, it encompasses all investors that do not own enough assets to be on the radar of traditional wealth managers or investors that are too cost sensitive to use their services.

However, despite this very general appeal of the idea behind the product, there is a more nuanced approach to understand which clients Wealthfront is targeting.

Wealthfront interface to manage client’s portfolio

On one hand “reluctant DIY’ers”, individuals who have a preference for some aspect of a human financial advisor but do not have the necessary assets for such a service.

On the other hand “delegators”, individuals willing to save and invest money, but nevertheless comfortable with delegating this activity to an automated service.

Launched in the Silicon Valley, an environment that is inherently tech savvy and open to innovation, it is understandable that Wealthfront’s primary targets are the “delegators”.

Initially, Wealthfront had focused on Millennials, a demographic that reflects the criteria of “delegators” particularly well for various reasons ranging from lack of interest or knowledge regarding financial matters, to distrust in the traditional financial institutions, all the way to their preference for products that cater to their desire of being empowered.

This approach to client segmentation is also a good starting point in order to understand why Wealthfront is particularly well suited to the address the initial problem.

Millennials represent a market with increasing importance but also a target that traditional players struggle to connect to. In addition, many in the wider population have lost their trust in traditional financial institutions after the financial crisis of 2008.

Focus on a fully automated investment service

Wealthfront was among the first companies to address this growing market by offering a cheaper, innovative product with superior service and high user-friendliness. In the eyes of the customer, their focus on a fully automated investment service clearly differentiates them from the traditional competition.

By combining both financial experts and Silicon Valley’s best technology talent they position themselves as an innovative company representing the future of financial services. In combination with their superior service this creates a brand that people are confident to trust in.

The trust of the clients manifests in the strong growth of Wealthfront’s assets under management over the last couple years. At the end of 2015 the company was managing about $3 billions of investments with a monthly growth rate of 5%.

In order to generate revenue, Wealthfront relies on a rather traditional model, earning 0.25% on all assets managed and interest on deposits.

According to estimations, the company’s annual revenues total $7 million while costs are between $40-50 millions.

While this situation can be attributed to the initial losses required to support growth (j-curve), Wealthfront will have to tap into additional customer segments and create new revenue streams in order to continue their growth.

In this regard, in addition to continuous improvements to their infrastructure, further innovations on the front-end seem to be of particular interest as Wealthfront has started integrating payment applications like Venmo.

Finally, in the increasingly competitive market of robo-advisors, innovations at the intersection of the different fields of the fintech ecosystem, like the use of social physics during the creation of investor profiles, could be a way to further strengthen Wealthfront’s future value proposition.

: une belle opportunité pour les fonds d’investissement à la recherche de LPs")