Techfoliance and The Fintech Twins are now travelling together to meet game changers in finance around the world. We want to help you understand the potential that these technologies could have in people’s life in every part of the world.

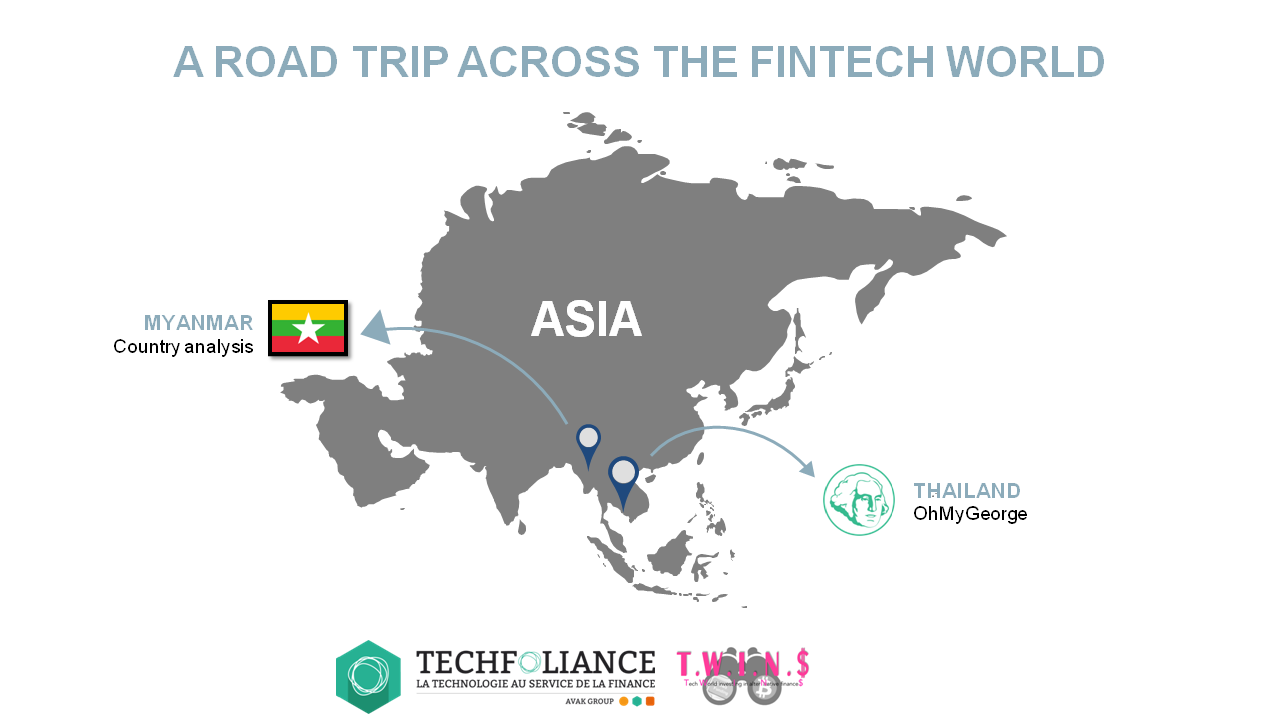

You would agree that the challenges for the Fintech sector are simply not the same between emerging and developed countries. That is why The Fintech Twins decided to travel to Myanmar in order to better understand why mobile banking could have a huge impact in this particular country ? Why is it the right time for financial inclusion in Myanmar ? Is the population ready to access this kind of services ?

They met entrepreneurs and went on to ask directly to the burmese to know more about the financial sytem, here is what they discovered :

Fintech in Myanmar – Key figures

MYANMAR

60 million people are living in Myanmar

47% of the popluation is under 24 years old

MOBILE INCLUSION

4th-fastest growing market for mobile phones in the world

Techfoliance initiated a Fintech Road Trip almost 3 months ago to meet entrepreneurs in finance across the world that are about to revolutionize the way people pay, invest or lend their money.

We already met Fintech start-ups in more than 10 countries coming from Europe, Africa and Asia. We discovered new technologies dedicated to the unbanked part of the world population that will allow them to pay or transfer money to their family and friends using their mobile phone. Or other technologies that will make capital markets accessible to everyone.

3 months after the beginning of our Fintech Road Trip

We are very glad to announce that we are joining The Fintech Twinsto bring you the best of financial innovation !

[one_half]

[/one_half]

[one_half_last]

[divider] THE FINTECH TWINS [/divider]

It is the story of chloé and marine, two twin sisters who used to work in finance : one in London, the other in Sydney. Seeing more and more disruptive start-ups being created in finance, they noticed that very few people were understanding what was the real impact of these new technologies in their lives.[/one_half_last]

In order to better understand what was really going on in the traditional financial system, the two sisters decided to embark on a 7 month journey to discover the many faces of alternative finance across Asia-Pacific.

By joining forces, Techfoliance and The Fintech Twins want to map the FinTech ecosystems in different places in the world and empower innovative game changers. Everything is going so fast that most people can’t have a clear overview of the revolution happening in the payment, lending, investment and many other sectors !

We want to make it fun and accessible to everyone. It is time for you to embark with us on this crazy, disruptive and human experience that will change our lives !

This is our 3rd stop in our Fintech Road Trip. To celebrate, our team met Lucien, the founder of OhMyGeorge!, a Bangkok-based Fintech that makes trading accessible to everyone :

[one_half][divider] The company [/divider]

OhMyGeorge is a financial trading game simulation featuring a level-up system that aims at making investing accessible, unintimidating and fun. The app lets you assess your risk appetite, analyse your investment behaviour and improve your emotion management skills. The team is taking its inspiration from Candy Crush and Zelda. Founded in 2015, the start-up is based in Bangkok.

[/one_half]

[one_half_last][divider] The entrepreneur [/divider]

Lucien Tavano is the founder of OhMyGeorge. Lucien graduated from ESSEC Business School and then worked during two years and a half as a corporate sales executive at Stelia Aerospace in Bangkok. He is interested in bringing to life innovative, fun and/or crazy ideas while building millennial-friendly company cultures.

[/one_half_last]

We headed to Bangkok to meet the team behind OhMyGeorge, a Fintech mobile-app still in beta testing with full of potential.

We are in a café, it is Tuesday the 22nd of March – 17:00 local Time

[divider] The Interview [/divider]

TECHFOLIANCE

Hi Lucien, we are very glad to meet OhMyGeorge today !

LUCIEN

Hi Techfoliance, that’s pretty cool that you stopped to Bangkok (laugh) to meet us.

We met you in Paris during a pitch session and we have to admit that you were the one that caught our attention. You’ve already created such a strong company culture…. Can you tell us a bit more about the story of OhMyGeorge ?

LUCIEN

Thanks for your kind words. Well, I decided to create OhMyGeorge after I got fed up of not being able to find a sustainable trading strategy despite my repetitive attempts. The interface of the trading platforms were sort of responsible for it. At the same time I was amazed by the level of emotions trading could provide, and being a gamer at heart, I saw the potential for the gamification of that environment. And that’s the DNA of the brand, “Oh My George!” translates the emotion you have when you “play” with your money, even if it’s just $1 (Ed. the face that appears on the 1-dollar note is George Washington’s).

[/tab]

[tab]

TECHFOLIANCE

So your strategy compared to most actors on the market (such as Robinhood) is to approach trading as a game, right ? We love that !But you agree that your early-stage adopters won’t be Mr. ‘Tout le monde’ : What target do you want to reach with OMG ?

LUCIEN

We are building OhMyGeorge for the mobile-first generation, who prefers to go to its dentist than listen to its bank (71% of US millennials). With our little casual game, we want to bring that generation to the financial markets and take it from day trading (the most appealing way to be involved in the market for a beginner) to investing (yes, it’s a long way) and even planning for their retirement. Ultimately, we want to create a mass market household brand in the financial services sector that people actually trust and love, and we think a gaming brand is the right angle to achieve that.

[/tab]

[tab]

TECHFOLIANCE

Your team is a fantastic example of the new generation of startupers : you have ‘no home’ because you want to work from everywhere (sometimes in Bangkok, sometimes in Singapore or in Paris) and your team comes from everywhere because you know that in 2016 you can work with talented people from around the world. However, you started launching your business in Asia instead of US or Europe : What are the main advantages you have to create a Fintech in Asia ?

LUCIEN

Most of the time, availability of capital is key to launch your start-up. Asia is currently seeing a massive availability of early stage venture capital. I remember a Singaporean VC explaining that they have so much money they can’t find enough good startups to invest in. Interestingly, it doesn’t matter much if you are based in Tokyo, Beijing, Taipei, Bangkok, Singapore, or Jakarta. In Asia, VCs are regularly touring the region, so you can catch them anywhere. At the same time, the lower cost of living, especially in Thailand, enables founders to bootstrap significantly longer than if they were building their company in the US or Europe. So we are really winning on both aspects.

OhMyGeorge being at the crossroad of FinTech and Mobile Gaming, we also chose Asia as a base and “domestic” market because mobile gaming is strong in that region: there are about 750 million mobile gamers in APAC, who spend almost as much money on mobile games (more than $4 per month per paying user) as Europeans do, despite a lower purchasing power.

[/tab]

[tab]

TECHFOLIANCE

You said you wanna create a strong enough corporate culture to make people feel confortable with finance : How do you think you will change people’s lives with OMG ?

LUCIEN

Our goal is to bring to the financial markets the Y generation, a generation that grew up during the 2008 crisis, and which as a result both distrusts these markets and lacks financial knowledge. Investing on the financial markets is the most liquid investment solution available, well-suited to rapidly-changing life conditions, millennials love that, since they hate to commit or to plan. With gaming, we will be perfectly positioned to attract, educate and orientate the general public to the right products or service providers.

[/tab]

[tab]

TECHFOLIANCE

Studies show that most people don’t know that new financial solutions are designed to fit their needs and expectations : According to you, what is the best way to make people better understand the sector of Fintechs ?

LUCIEN

Gamification? Ahah, no but seriously, we need to talk in familiar terms and by similarities. Let’s face it, FinTech is at the end of the day just a fancy word, because almost all companies in that sector are tech by nature, some are just more modern than others as they enjoy the privilege of not having a technological debt.

Ultimately, FinTechs are financial companies for the modern life. I am currently trying to have some money wired from my French bank account to a Hong Kong-based service provider I contracted (note: Hong Kong is not an IBAN country…). It’s been 10 days, and after 2 emails, a visit to the closest agency of my bank, and 2 phone calls I still have no idea when my transfer will be executed or how much it will cost me (!!!). I wish we were already 5 years in the future and my contractor could accept TransferWise.

[/tab]

[tab]

TECHFOLIANCE

We are used to asking each start-up if they have an anecdoteto deliver about their company : something funny, difficulties you have faced, the team, etc.

LUCIEN

I can’t be too specific on that one, but I can say we got in bed too quickly with the wrong partner for our startup at a very early stage of our formation, and until we ended that relationship it literally drained our energy and focus. But at the same time, it really helped forged a strong, cohesive team.

Fun fact : we actually have “hidden co-founders” (a.k.a. our girlfriends) who support our mood swings and are our beloved beta testers (read “guinea pigs”). The truth is, the stats have spoken, they are actually better than us at OhMyGeorge !

[/tab]

[/tabs]

OPPORTUNITIES

Wanna go to Bangkok to work with a talented and dynamic team ? You don’t believe us that you could work in better condition in a startup ? Checkout the pic’ below :

Ouch, we agree with you, it hearts to feel that some people are trying to change the world in that kind of condition 😉

WHAT’S NEXT ?

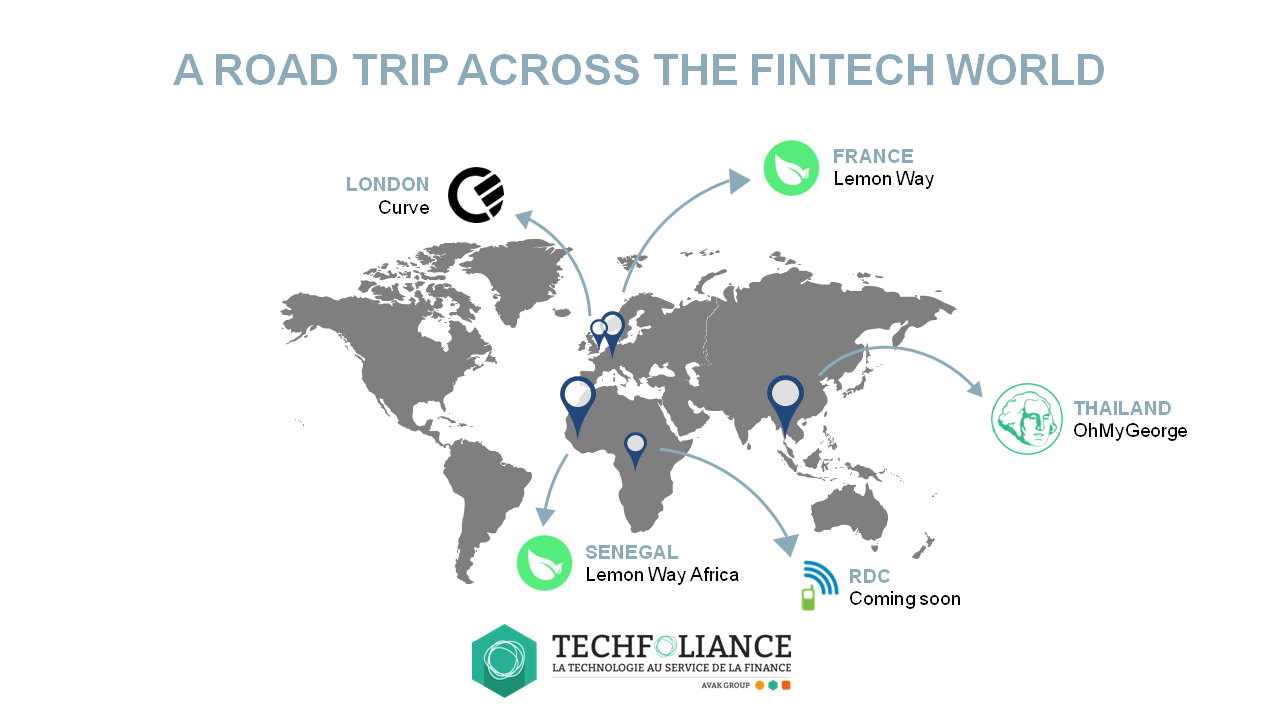

We conclude our interview here. We hope you enjoyed discovering this amazing start-up ! Follow us on our quest accross the world of Fintech and see on the map what will be our next stop :

A Road Trip Across The Fintech World – Congo

Stop 1 : France – Lemon Way – Payment Service Provider for Marketplaces

Each month, our team pick-up five figures about Fintech that you must know to better understand the magnitude of the disruption going on in the financial world. This month, we highlight Fintech in Mexico, total investment made in Fintech, Blockchain, Africa and robo-advisors :

FINTECH FIGURES OF THE MONTH

In 2014, only 38 million dollars were invested in Fintechs in Mexico

In december 2015, Fintechs around the world have raised almost 1 billion dollars in 1 month

40 of the biggest banks in the world have joined the consortium R3CEV to deal with the Blockchain revolution

Interswitch, a start-up that develop payment solutions in South Africa, could become the first african unicorn valued at 1 billion dollars

According to Bank of America studies, robo-advisors’ market will be valued at 130 billion dollars up to 2020

Betterment, the most funded robo-advisor in the world

More and more investments are allocated into robo-advisors, algorithms developed to make wealth management affordable for everyone.

With an additional 100 million dollars, Betterment is officially the most funded robo-advisors in the world with almost 205 millions dollars raised since 2010. Followed by Wealthfront with almost 130 million dollars raised, Motif investingwith 127 million dollars andPersonal Capitalwhich raised 100 million dollars.

Note that the Top 5 of the Robo-advisors in the world are all american.

The New-York-based ‘start-up’ which is now valued at 700 million dollars has more than 150 000 clients on its platform and manages almost 4 billion dollars of assets.

Historical VC funds such as Anthemis group, Bessemer venture partners, Francisco partners or Menlo Ventures have contributed to the Serie E round and welcomed the arrival of the stockholm-based fund Kinnevik that led the round.

Kinnevik had already invested minority stakes in two Fintech start-ups : Bima, a solution to provide people in emerging countries with insurance and Bayport, a solution to provide financial services in Africa and Latin America.

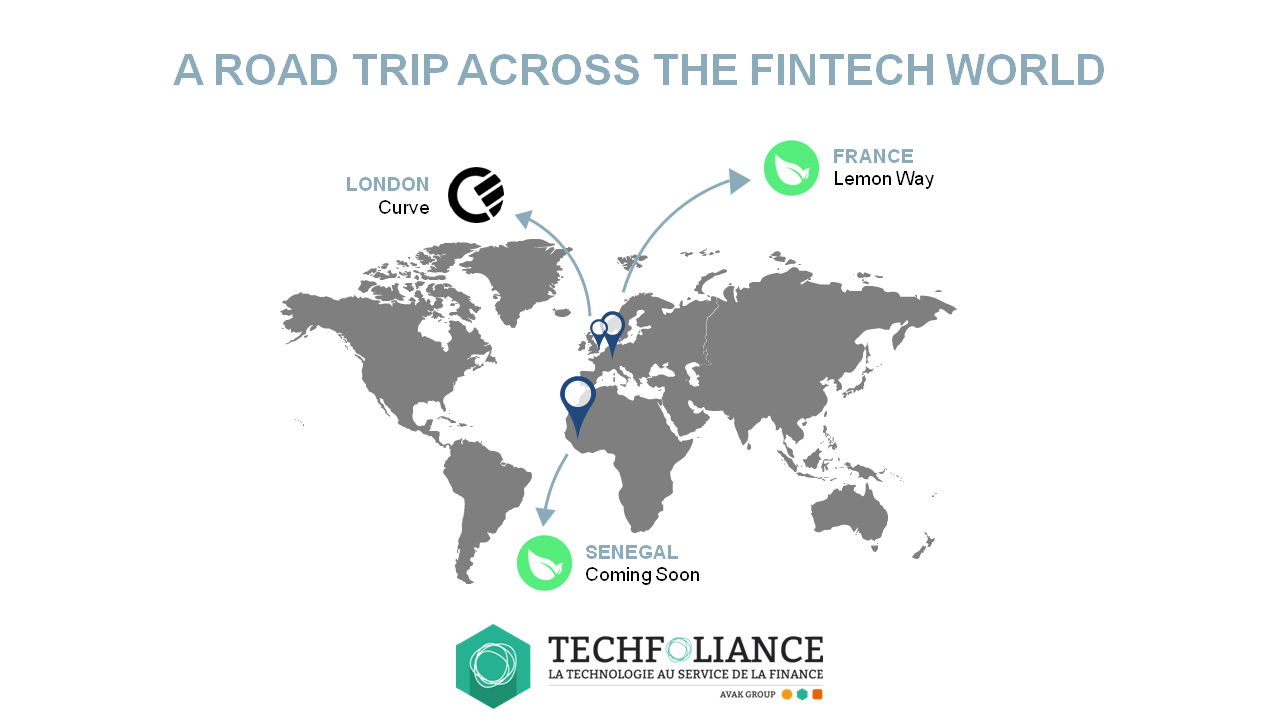

Our team met Anna, one of the three co-founder of Curve, a London-based Fintech that is changing the way we pay with our credit cards :

[one_half][divider] The company [/divider]

Curve combines a person’s credit and debit cards into one single payment card which is accepted everywhere MasterCard® works, with Chip and Pin, magstripe and Contactless technology. By uniting existing cards in a single place, users access low foreign exchange rates with no fees, see and label transactions from all accounts in one screen in real-time and can pay with American Express in places it isn’t accepted. Curve puts users back at the centre of their financial world, without changing their behaviour or bank.

[/one_half]

[one_half_last][divider] The entrepreneur [/divider]

Anna Mostyn Williams is Marketing Lead and Co-Founder at Curve. Anna graduated from an MBA at INSEAD and then worked during 2 years at Microsoft as a Senior Product Marketing Manager. She co-founded Curve in May 2015 after discussing with Shachar Bialick and Tom Foster-Carter, who also graduated from INSEAD, about the need to bring new payment solutions to customers. The meeting of these three brillant mind has allowed to create Curve, one of the hottest Fintech start-up in London that we are very proud to introduce you today.

[/one_half_last]

[divider] The Interview [/divider]

It has not been easy to schedule an interview since everything is going fast for this young start-up : product launch, fundraising, recruitment etc. In that sense, we deeply want to thank them for their time. Here is the story of an amazing Fintech : Curve.

Wednesday the 9th of March – 10:30 local Time

TECHFOLIANCE

Good morning Anna, many thanks for taking some of your time to introduce your company to our readers !

ANNA

Hi Techfoliance, we are very glad to spread Curve’s revolution with your community.

TECHFOLIANCE

We are truly impressed with what you’ve achieved so far with Curve. The technology is now available in 35 million places, you raised 2 million dollars from top entrepreneurs such as Taavet Hinrikus (Co-founder Transferwise) or Ricky Know (Co-founder Azimo) …. Can you start telling us the story of your company ? Why and how did you decide to create Curve ?

ANNA

Thank you so much ! We like to think of Curve as the rebundling of banking services. What does that mean ? Over recent years the deregulation of financial services has led to multiple players entering the space, all disrupting services that were traditionally provided by banks – which has been amazing. But this has led to the continued fragmentation of the financial landscape – as a user I still have to use multiple services by different providers – I carry different cards in my wallet – for payments, for loyalty, I use another service for investments, another for foreign transfers – and so forth and so on. We don’t believe this is putting the user first, so have set out to ‘rebundle’ banking services, and put users back at the centre, by using one card and one phone app, to provide one single access point to multiple services.

TECHFOLIANCE

So the idea with Curve is to continue the service always keeping the user at the centerpoint, right ?Couldyou now explain us more concretelyhowdo you facilitate people’s lives with Curve ?

ANNA

That’s right. You use the Curve app to upload your existing payment cards and link them to your Curve card. Choose which card you want to charge, and you’re ready to go and pay with your Curve card – simply leave all your other cards at home. It is easy to change which card gets charged – just open the Curve app and tap to change. Users access multiple benefits. They see all their transactions across all their accounts, in one screen in real time. They can easily export these transactions to csv format, and all photo and log receipts on the go, adding them to each transaction. We allow users to use Amex and collect their points in places it isn’t accepted, and eliminate existing cards FX fees, cutting them to the MasterCard rate + a transparent 1%. (checkout the video to see how it works)

TECHFOLIANCE

What differentiate Curve from most of the Fintechs companies that we have seen over the past months is that compared to most of them you don’t compete with banks but instead you work with them. Can you tell usthe relation you have with banks and how did they welcome your arrival on the market ?

ANNA

We are not trying to get rid of the banks, we layer on top of their services to make the user experience seamless and efficient. Leave your money safe with them, as a deposit, but use our services to get control and clarity over your spending, and eliminate all those unnecessary fees and charges.

TECHFOLIANCE

So you said that the service was free for customers and that the user is not charged when he / she withdraw cash. How do you make money then ?

ANNA

We charge upfront for the card – £35 for the blue card, £75 for the black card. This is a one off payment.

TECHFOLIANCE

What is fascinating with Curve is that you are probably the first actor on the market to approach payment in the way you do, that is carrying out all your cards in one ! I guess your direct competitors could be the mobile payment actors. Do you see them as competitors ?

ANNA

You are right, mobile payment actors could be seen as our main competitors. They have the ability to do what we do. However, there are currently several issues which hamper mobile payment adoption. You have to use your mobile (of course!) – which people are not accustomed to, and the merchant has to accept contactless payments (less than 5% worldwide). There is also a cap on the amount you can pay with your mobile – £30 in the UK. This is not the case with Curve. We wanted to give the benefits of what we’ve seen in mobile payment but by using the humble bank card, which people are accustomed to – having carried them in their pockets for the last 50 years

TECHFOLIANCE

Recent studies in UK have shown that 53% of people don’t use Fintech services simply because they did not know they existed. Would you have a point of view on how to make people be aware and understand what Fintechs are all about ?

ANNA

That may be true, but I think FinTech is rapidly entering the mainstream, and it is an incredibly exciting time to be part of it. Of course you have to use the relevant marketing channels to drive mass market awareness, but fundamentally you also need a product / service that solves a tangible issue for the end user – a product that will help users with their day to day lives. In an ideal world the product should be your strongest marketing tool – as you want users to tell their friends, who tell their friends, who tell their friends, and that way, you’ve created natural evangelists.

OPPORTUNITIES

If you loved Curve and think that you would be ready to stop everything to go and work with this brillant team, feel free to go to FIND YOUR DREAM JOB AT CURVE IN LONDON : they are looking for talented people to join the team !

WHAT’S NEXT ?

We conclude our interview here. We hope you enjoyed discovering this amazing start-up ! Follow us on our quest accross the world of Fintech and see on the map what will be our next stop :

A Road Trip Across The Fintech World – Senegal

Stop 1 : France – Lemon Way – Payment Service Provider for Marketplaces

: une belle opportunité pour les fonds d’investissement à la recherche de LPs")